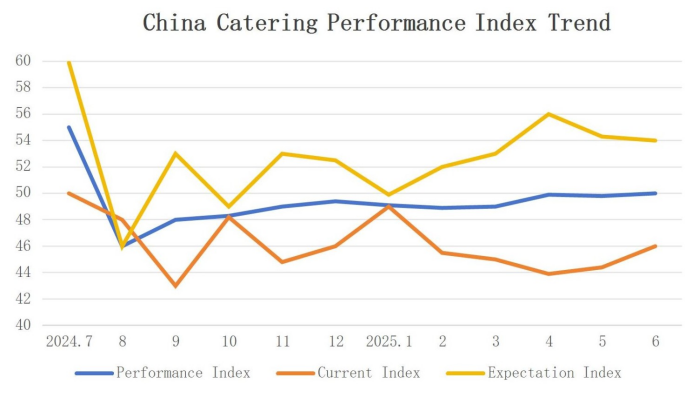

China's Catering Industry performance index Report for June Released Two Indicators Approach Critical Threshold

Recently, the China Cuisine Association released the China Catering Industry performance index (CRPI) report for June. The CRPI consists of two dimensions—current index and expectation index—comprising 10 indicators. According to the report, the catering industry's performance index for June was 49.98, up by 0.56. Since August 2024, the index has shown minor fluctuations, gradually approaching a neutral level. The industry has continued a slight contraction trend for nearly 11 months, currently in a phase of overlapping influences from overall recovery and structural adjustments.

Significant Increase in Customer Traffic Index

The current index for June was 45.84, up by 1.23 month-on-month. Among the sub-indices, the store profitability index was 46.16, and the customer traffic index was 49.23, up by 1.56 and 5.78 respectively month-on-month. Meanwhile, the store sales index was 43.30, and the employment scale index was 44.65, down by 2.01 and 0.44 respectively year-on-year.

Among all indicators for the month, the customer traffic index saw the highest increase, but the store sales and profitability index did not rise correspondingly. This reflects that although more customers visited, the average per customer spending decreased, which is attributed to intensified market competition, changes in consumer habits, and ongoing sales promotion.

The expectation index for June was 54.12, down by 0.10 from the previous month. Among the sub-indices, the store profitability expectation index was 56.06, and the customer traffic expectation index was 56.46, up by 0.01 and 5.04 respectively month-on-month. The store sales expectation index was 55.77, and the employment scale expectation index was 50.42, down by 2.31 and 0.17 respectively. The investment expectation index was 51.9, and the quarterly expectation index was 61.41.

Notably, the employment scale expectation index and investment expectation index are approaching the critical threshold, indicating that some catering enterprises face certain pressures and challenges in expansion and workforce allocation.

Analysis of Performance Differences by Scale and Business Type

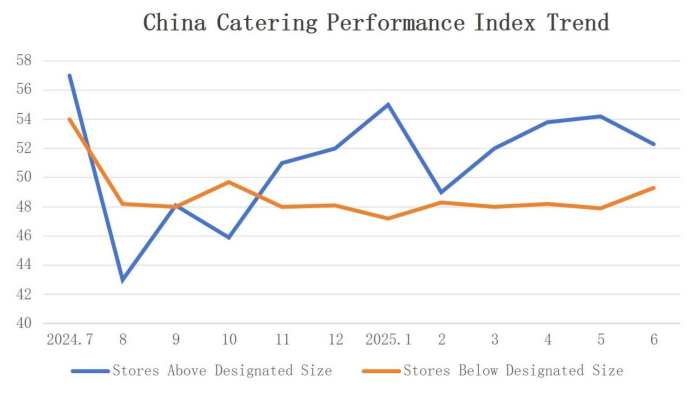

In June, the performance indices of catering businesses of different scales showed opposite trends. The performance index for large-scale stores (above the designated size) was 52.34, down by 2.02 month-on-month. Among them, the current index was 46.74, down by 6.88, while the expectation index was 57.95, up by 2.84. The performance index for small-scale stores (below the designated size) was49.19, up by 1.42 month-on-month, with the current index at 45.53 (up by 3.92 month-on-month) and the expectation index at 52.85 (down by 1.08 month-on-month).

In June, the current index for large and small stores were 46.74 and 45.53 respectively, showing close proximity. Recent intensified online and offline promotions have further heightened consumers' price sensitivity. Small stores, leveraging their flexible business models, are better positioned to capitalize on short-term consumption booms by offering discounted combos or specialty snacks, thereby boosting customer traffic and sales. In contrast, large stores may face lower flexibility in adjusting strategies due to their scale, along with higher operational pressures during the summer season, such as staffing and supply chain management, leading to increased costs and squeezed profit margins, which contributed to the decline in their current index.

The expectation index for large stores in June was 57.95, up by 2.84 year-on-year, with all indicators above the neutral level. Except for the store sales expectation index, the profitability, employment scale, and customer traffic expectation index all rose simultaneously. For small stores, the expectation index was 52.85%, down by 1.08 year-on-year. Except for the employment scale expectation index, which was below the neutral level, all other indicators remained above it.

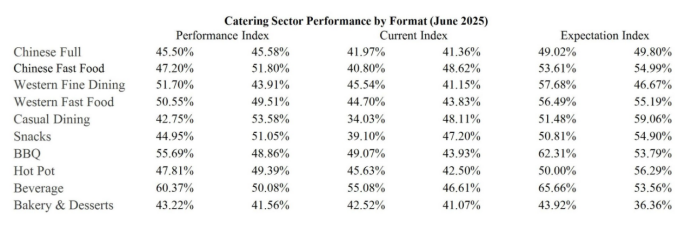

Among all formats, Chinese fast food, casual dining, snacks, and beverages outperformed in June, with performance indices of 51.80, 53.58, 51.05, and 50.08 respectively, all above the neutral level. Their expectation indices also exceeded 53, indicating a sustained positive trend. The current performance indices for Chinese fast food, casual dining, and snacks rose by 7.82, 14.08, and 8.10 respectively, driven by summer peak periods of consumption, consumer’s health trends, and platform promotions. In contrast, Western full-service dining and bakery/dessert sectors underperformed, with indices of 43.91 and 41.56, significantly below the neutral level, due to the joint influence by changing market conditions, competitive situation, and seasonal fluctuations, etc.

Optimistic Outlook for Summer Catering Market

Overall, the catering industry's performance index for June was 0.02 below the neutral level, reflecting persistent challenges but an upward trend.

By index dimension, the current index rose but remained below neutral, while the expectation index dipped slightly but stayed above neutral. Since August 2024, the current and expectation indices have shown divergent trends. In June, these indices converged, indicating that despite operational pressures, the industry remains optimistic about the summer catering market.

By scale, large stores exhibited greater volatility over the past 12 months but stabilized slightly above neutral since March while small stores remained slightly below neutral. This suggests that large stores are more sensitive to market changes and demonstrate greater foresight in formulating response strategies. Leveraging their scale advantages and resource allocation capabilities, they can proactively plan promotional activities for holidays and peak seasons. On the other hand, due to small store’s smaller operational scale, they can quickly adjust their business strategies—such as optimizing workforce structures or introducing specialty dishes and services—to adapt to market shifts. This flexibility allows them to respond swiftly to market fluctuations, minimizing losses and maintaining basic operational stability.

By format, Chinese fast food, casual dining, and snacks stood out in June, partly due to seasonal factors.

By investment and quarterly expectation indices, although the catering industry has been in a state of prolonged micro-contraction, both indices have stayed above neutral for 12 consecutive months, suggesting that, amid policy support and a broader market recovery trend, businesses and stores maintain an optimistic attitude toward investment and remain confident in the future development prospects of the catering industry.

'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1477_4631'%20x1='18.272'%20y1='0'%20x2='18.272'%20y2='35.3674'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23FF9F9F'/%3e%3cstop%20offset='1'%20stop-color='%23F15E5E'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1477_4633'%20x1='17.5'%20y1='0'%20x2='17.5'%20y2='35'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23E9C0EE'/%3e%3cstop%20offset='1'%20stop-color='%23CE57DC'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)